How many times have you looked at your bank statement and noticed a random ₹199, ₹299, or ₹499 deduction, only to realize it was for an app you haven’t opened in months?

I am Ishwar Bulbule. During my five years working at ICICI Prudential and over 14 years actively investing in mutual funds, I have noticed a fascinating contradiction. Most Indian investors will spend hours checking the daily NAV (Net Asset Value) of their mutual funds to ensure their wealth is growing. Yet, these same smart investors completely ignore the silent wealth-killers hiding in their credit card statements.

Today, we are going to tackle a modern financial disease called Subscription Fatigue. As we step further into 2026, the digital world is designed to make you pay effortlessly and forget instantly. In this article, I will not give you any “get-rich-quick” shortcuts or vague stock tips. Instead, we will look at hard data, simple mathematics, and actionable strategies to plug the holes in your financial bucket.

By the end of this guide, you will learn exactly how to identify these invisible drains, reclaim your cash flow, and redirect those funds toward building a solid retirement corpus. Let’s dive in.

What is Subscription Fatigue and How is it Harming You?

![]()

When you sign up for multiple digital platforms—such as OTT services, music apps, fitness trackers, food delivery memberships, and premium software—and managing them becomes financially and mentally exhausting, you are experiencing Subscription Fatigue.

The Indian consumer market has fundamentally shifted from an “ownership” model to an “access” model. Ten years ago, we bought CDs or DVDs; today, we rent access to Netflix or Spotify.

The Illusion of Micro-Transactions

When an app charges you just ₹199 a month, your brain categorizes it as a negligible expense. We call these “micro-transactions.” However, when you stack Amazon Prime, Swiggy One, Zomato Gold, YouTube Premium, a gym membership, and a cloud storage plan, that small number easily balloons to ₹2,000 to ₹3,000 per month.

According to the latest 2025-2026 IAMAI report, India’s internet user base has officially crossed 950 million. Internet access has become incredibly cheap, but the services riding on it are slowly draining our wallets.

Paying for What You Don’t Use

The real harm comes from non-usage. A March 2026 report by Sensor Tower revealed that streaming fatigue has hit India hard, with the time spent on OTT platforms dropping by 16% compared to previous years.

This means people are spending less time watching shows, but their monthly auto-debits are still active. You are essentially paying companies for a service you are not consuming. In the world of finance, this is a direct attack on your investable equity and severely limits your ability to build a robust portfolio.

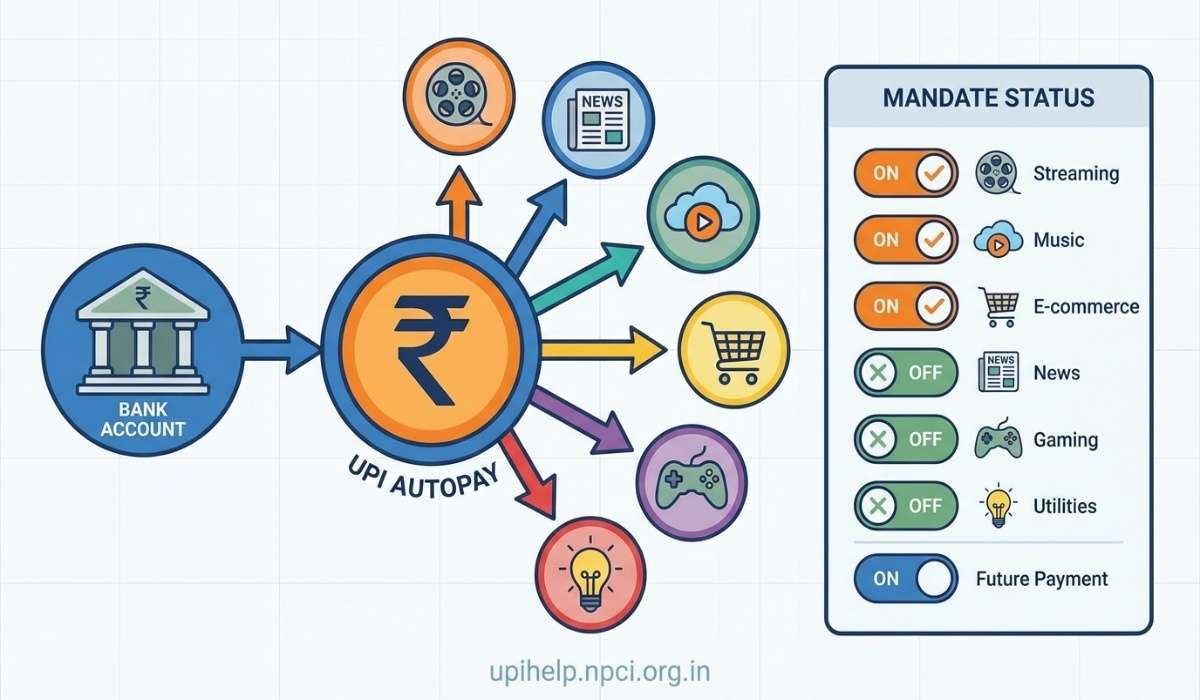

UPI Autopay and E-mandate: Convenience or Warning Bell?

Over the past few years, digital payments in India have become incredibly frictionless. The introduction of UPI Autopay by the NPCI (National Payments Corporation of India) revolutionized how we buy subscriptions. With just one click and a UPI PIN, you are locked in.

When you sign up, you create an E-mandate. This is a standing instruction to your bank saying, “You have my permission to deduct this specific amount every month without asking me.”

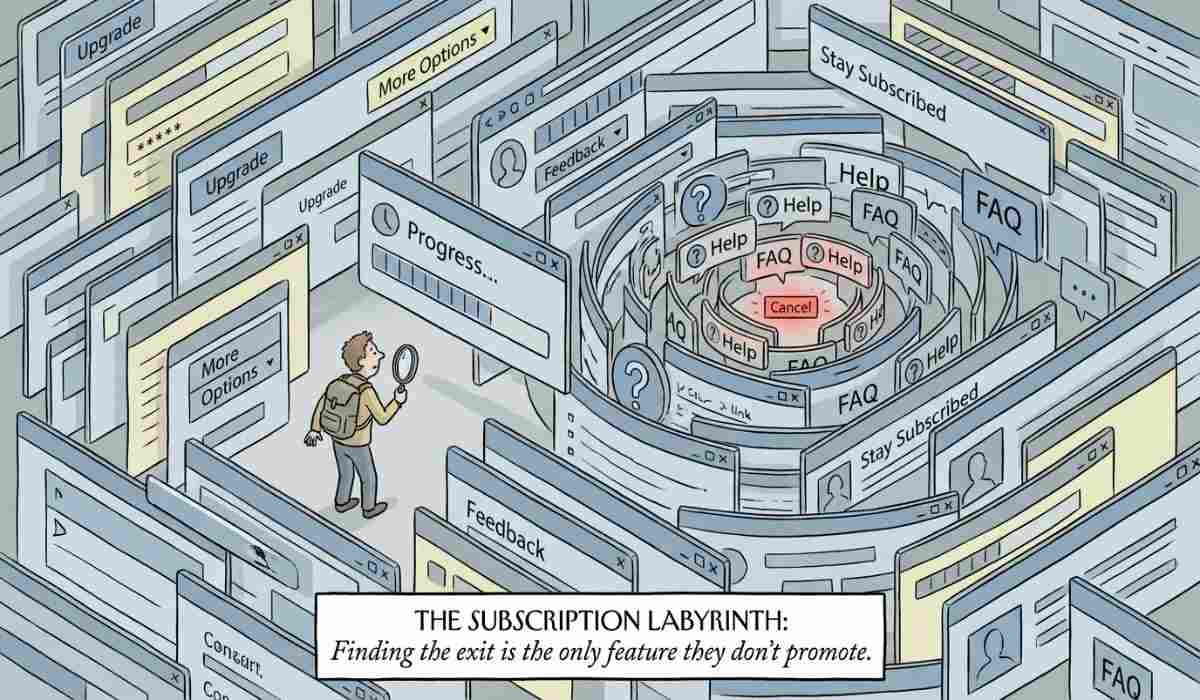

The Trap of “Dark Patterns”

While Autopay is highly convenient, it brings a massive hidden risk. Many tech companies use “dark patterns.” They make the subscription process take exactly ten seconds, but they bury the “Cancel Subscription” button deep inside a complicated web menu. Sometimes, it is entirely missing from the mobile app.

During my time analyzing client cash flows, I saw this firsthand. A well-paid IT engineer client of mine had a recurring E-mandate for a premium fitness app. He paid ₹499 every month for three years. When we audited his finances, we found he had only used the app twice. He effectively threw away nearly ₹18,000 simply because cancelling the mandate felt like “too much work.”

Regulatory Lifelines for Consumers

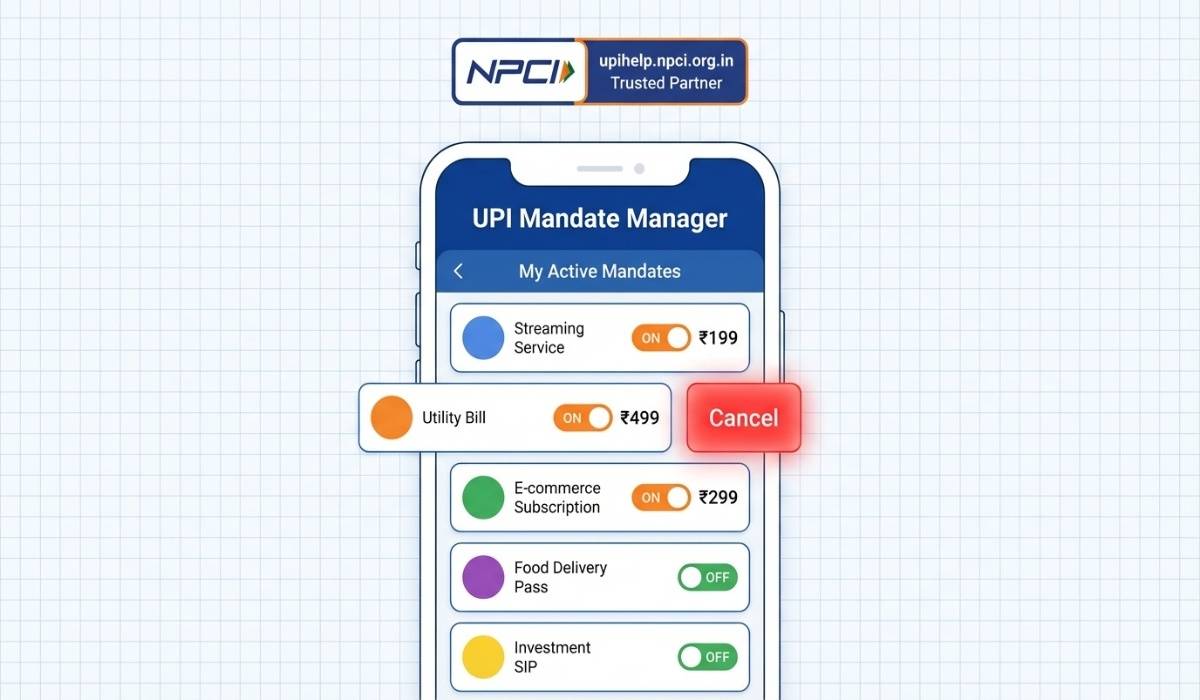

Fortunately, the Indian regulatory system has stepped up. To combat these opaque billing practices, the NPCI launched a centralized portal in December 2025: upihelp.npci.org.in.

This platform allows any user to log in and instantly view all active UPI Autopay mandates linked to their phone number. More importantly, you can cancel any unwanted subscription directly from this portal with a single click, completely bypassing the merchant’s complicated cancellation process.

Small Amount, Big Loss: The Reverse Effect of Compounding

Albert Einstein famously called compounding the eighth wonder of the world. He noted that those who understand it, earn it; those who don’t, pay it.

When you invest in a SIP (Systematic Investment Plan), compounding works in your favor to multiply your wealth. However, subscription fatigue operates as “reverse compounding.” Every rupee that leaks out of your bank account is a rupee that loses its future earning potential.

Let’s look at the numbers. Imagine you have five subscriptions that you rarely use:

- OTT Platform 1: ₹199/month

- OTT Platform 2: ₹299/month

- Food Delivery Membership: ₹150/month

- Premium Music App: ₹99/month

- Unused Fitness/Software App: ₹500/month

Total Monthly Waste: ₹1,247. Let’s round this off to ₹1,500 for easy calculation.

The Real Cost of ₹1,500

What happens if you cancel these unused services and redirect that exact ₹1,500 into a broad market index fund tracking the NSE Nifty 50 or the BSE Sensex? Historically, Indian equity markets have delivered an approximate long-term CAGR (Compound Annual Growth Rate) of 12%.

Here is the math over a 15-year period:

| Financial Action | Monthly Amount | Total Out of Pocket (15 Yrs) | Final Value (15 Yrs) |

| Keeping Unused Subscriptions | ₹1,500 lost | ₹2,70,000 | ₹0 |

| Investing in a Nifty 50 SIP (12% CAGR) | ₹1,500 invested | ₹2,70,000 | ₹7,56,000 |

By simply ignoring your bank statements, you aren’t just losing ₹1,500 a month; you are sacrificing over ₹7.5 Lakhs of future wealth. That is money that could have fully funded your child’s early education or served as a massive boost to your emergency fund.

Furthermore, high expense ratios in mutual funds can eat your returns, but a 100% loss through a forgotten subscription is the worst expense ratio of all!

3 Simple Steps to Break Free from Subscription Fatigue

If you want to stop this silent wealth drain, you need to take immediate action. Here is the exact three-step framework I recommend to all new investors looking to clean up their cash flow.

Step 1: Conduct a Brutal Financial Audit

Pull up your bank and credit card statements from the last 90 days. Grab a highlighter (or use a spreadsheet) and mark every single recurring transaction. Look for terms like “Auto-debit,” “Recurring,” or specific app names.

Next, log into the NPCI portal (upihelp.npci.org.in) and review your active E-mandates. You can also use expense tracker apps like INDmoney or Moneyview to categorize your past spending automatically. You will likely find at least two or three services you forgot you were paying for.

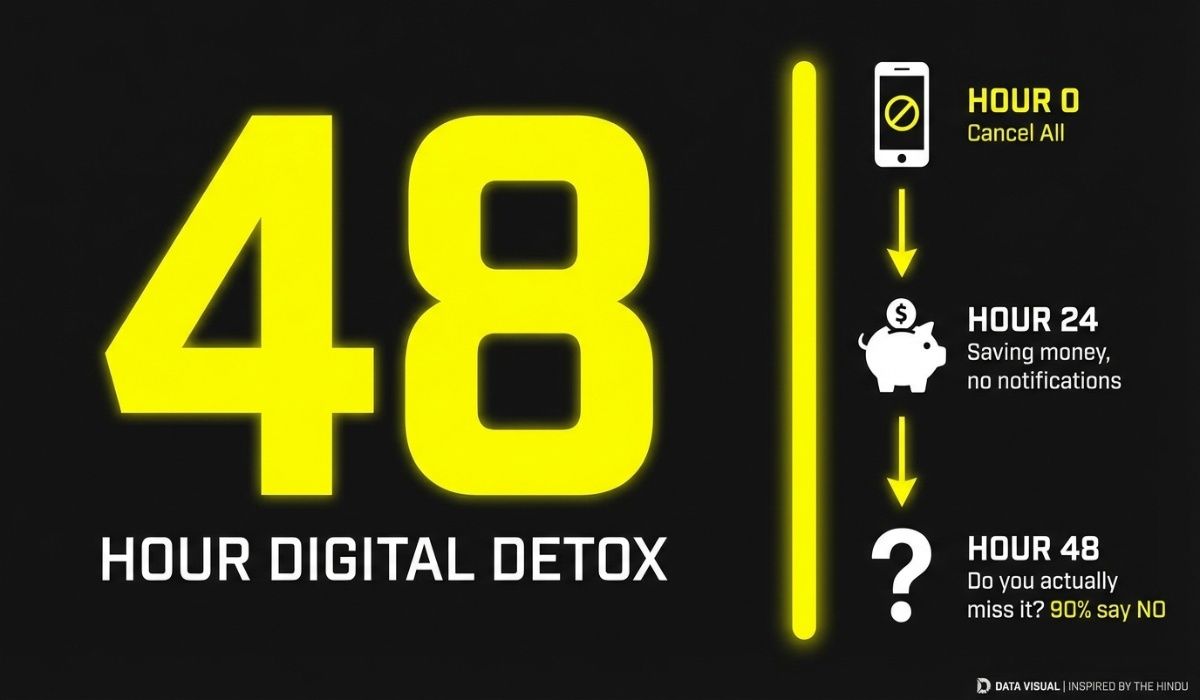

Step 2: Implement the 48-Hour Rule

This is my favorite behavioral finance trick. Cancel all your non-essential digital subscriptions today. Yes, every single one of them.

Once cancelled, wait. If you genuinely need a service—for example, a highly anticipated web series drops on an OTT platform—wait 48 hours before resubscribing. This forced pause eliminates impulse buying. You will quickly discover that you can easily live without 90% of the apps you thought were “essential.”

Step 3: Optimize Through Bundling

Instead of paying for six different apps, look for aggregated services. For example, subscriptions like Times Prime bundle multiple benefits (OTTs, food delivery discounts, music) into one single annual fee.

However, apply the concept of asset allocation to your spending. Just as you allocate your capital across different asset classes for diversification, allocate your entertainment budget strictly. Only pay for bundles if you actually use the majority of the services included. Otherwise, you are just paying a premium for clutter.

My Personal Formula: How to Manage Recurring Costs?

In my 14 years of investing and 5 years actively navigating the highly volatile cryptocurrency markets, I have learned that capital preservation is just as important as capital appreciation.

During my tenure at ICICI Prudential, I observed the habits of highly successful wealth builders. The individuals who thrived during market crashes were not those who picked the best stocks; they were the ones who had absolute control over their fixed monthly costs.

Here is my personal, data-backed formula for managing recurring expenses:

- Autopay is Exclusively for Wealth Creation and Protection: I only allow auto-debits for two things: my mutual fund SIPs and my term insurance premiums. Automating your investments enforces discipline. Automating your entertainment enforces laziness.

- Strict Manual Payments for Lifestyle Apps: I never attach an E-mandate to an OTT platform or a food delivery app. When a one-month subscription expires, the app will cut off my access and ask for payment. I treat this as a “checkpoint.” If I actually have the time and desire to watch something that weekend, I manually pay for exactly one month.

- Avoid Annual Traps: Many apps offer a “discount” if you pay for a full year upfront. Unless it is a tool I use for my daily business, I refuse annual plans. I do not know if I will have the time to watch a specific streaming service eight months from now. Flexibility is worth more than a 10% discount.

Your money is your most powerful tool. Do not willingly hand over the control of your cash flow to the automated algorithms of tech companies.

Conclusion

Building wealth is not just about finding the perfect stock or hunting for the highest returns. It begins with defending the money you already make. Subscription fatigue is the silent killer of the modern digital era, bleeding your cash flow dry one small transaction at a time.

Key Takeaways to Implement Today:

- Identify the Leakage: Small, recurring costs of ₹199 or ₹499 compound into massive long-term losses.

- Leverage the Math: Redirecting just ₹1,500 a month from dead subscriptions into a Nifty 50 index fund can generate over ₹7.5 Lakhs in 15 years.

- Take Back Control: Use the NPCI’s centralized portal (upihelp.npci.org.in) to find and cancel hidden E-mandates instantly.

- Protect Your Autopay: Reserve automatic bank deductions strictly for your SIPs and life insurance. Force yourself to pay manually for entertainment.

Your financial future depends heavily on the small decisions you make today. Open your bank app right now, audit your mandates, and cut the dead weight. Remember, every single rupee you save today is a soldier fighting for your financial freedom tomorrow!

Also Read: Can Thematic Funds Capture India’s Semiconductors & AI Infra?

Disclaimer: This article is for educational and informational purposes only. It does not constitute direct financial advice or a recommendation to buy or sell any specific mutual funds or stocks. Always consult with a SEBI-registered financial advisor before making major investment decisions.