Why do most Indian families lose money on physical gold despite treating it as their ultimate “safe” asset?

Think about it. You buy gold jewelry, pay high making charges, and then lock it away in a bank vault. Not only does this gold generate zero income, but you also end up paying annual locker fees to the bank just to keep it safe. According to macroeconomic estimates, Indian households and trusts hold over 25,000 tonnes of idle gold. That is nearly $2 trillion of wealth doing absolutely nothing.

Hi, I am Ishwar Bulbule. During my 5+ years at ICICI Prudential and over 14 years actively investing in mutual funds and the stock market, I have seen investors chase complex products while ignoring the gold sitting right in their homes.

Today, we are going to fix that. We will decode the Gold monetization scheme by Indian government and banks in 2026: HOW TO earn from physical gold. I will walk you through exactly how this scheme works, the massive regulatory updates that happened recently, and how you can use it to build a smarter financial portfolio.

Let’s turn your dead asset into a cash-generating machine.

What is Gold monetization scheme (GMS)?

The Gold Monetization Scheme (GMS) is a government-backed initiative designed to unlock the value of privately held gold. Launched initially in 2015 by the Indian Government and the Reserve Bank of India (RBI), the goal was simple: bring the country’s massive private gold reserves into the formal banking system.

Think of the GMS as a fixed deposit for your physical gold. Instead of depositing cash, you deposit your idle gold (like bars, coins, or old jewelry). The bank takes your gold, tests its purity, and opens a “Gold Savings Account” for you. From that day onward, your gold earns an annual interest rate.

Why did the government do this? India is the world’s second-largest importer of gold, bringing in around 800 to 900 tonnes every year. This massive import drains our foreign exchange reserves and hurts the Indian economy. By encouraging citizens to participate in the Gold monetization scheme by Indian government and banks in 2026: HOW TO earn from physical gold, the government can recycle domestic gold, lend it to jewelers, and reduce expensive imports.

In my experience advising clients on portfolio diversification, GMS is the only financial product that allows you to earn a yield on physical gold you already own, without forcing you to sell it permanently.

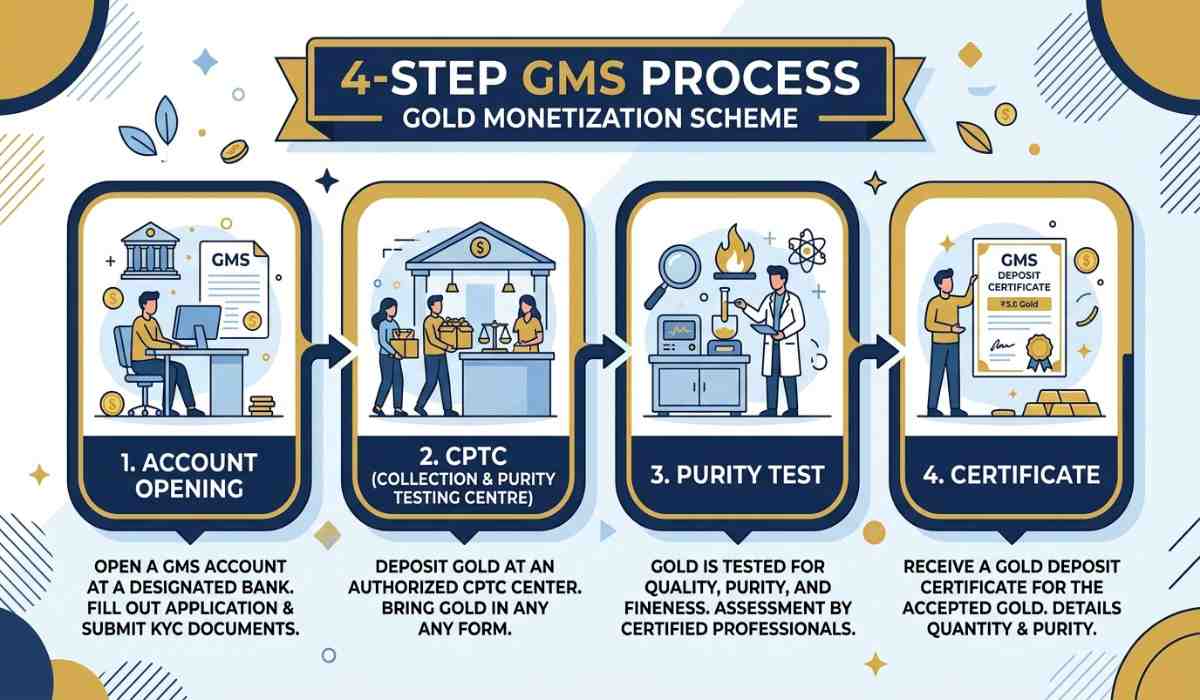

How It Works — Step by Step

Starting your GMS journey is completely different from starting a SIP in a mutual fund or buying equity shares on the BSE or NSE. Here is the exact step-by-step process you need to follow in 2026:

Step 1: KYC and Bank Visit

First, visit a designated bank branch that offers the GMS. You need to carry your standard KYC documents (Aadhaar card, PAN card, and passport-size photographs). You tell the bank you want to open a Gold Savings Account.

Step 2: Go to a CPTC

The bank will not test your gold. Instead, they will direct you to a government-approved Collection and Purity Testing Centre (CPTC). You take your physical gold to this center. The minimum deposit limit is just 10 grams of raw gold (this can be jewelry, coins, or bars, but stones and other metals are excluded).

Step 3: Purity Testing and Certificate

The CPTC will melt your gold to check its exact purity. If you agree to the purity results, they will issue you a deposit receipt or certificate stating the exact weight of 995-fineness gold you own.

Step 4: Account Activation

You take this purity certificate back to your bank. The bank officially opens your Gold Savings Account and credits the exact grams of pure gold to your ledger. Your interest calculation begins on this day.

Collection and Purity Testing Centre (CPTC)

The Collection and Purity Testing Centre (CPTC) is the heart of the GMS process. Because Indian jewelry comes in various purities (18K, 22K, 24K), banks cannot accurately value your deposit without a standard measure.

When you hand over your jewelry at the CPTC, they first do a preliminary X-ray fluorescence (XRF) test to give you an estimate. If you agree, they proceed to melt the gold. This is crucial: your jewelry will be destroyed. They melt it, remove any impurities, stones, or alloys, and convert it into standard pure gold.

I want to share a quick personal story. When I explained this scheme to my mother a few years ago, she flatly refused to deposit her wedding jewelry because of its emotional value. However, we found a middle ground. We gathered broken chains, old single earrings, and outdated coins that had no emotional value. We took those to the CPTC. Melting them was an easy decision, and it instantly started earning interest.

Never deposit jewelry that carries emotional or antique value into the GMS. Only use idle, unwanted, or pure investment gold.

Deposit Types — 2026 Update

If you read outdated articles on the internet, you will hear about Short, Medium, and Long-Term deposits. However, as an investor, you must stay updated with SEBI and RBI circulars.

In March 2025, the RBI made a massive regulatory shift. The government officially discontinued the Medium and Long Term Government Deposits (MLTGD). This means that in 2026, you can no longer lock your gold in for 5-15 years under the government-backed portion of the scheme. If you had an old MLTGD account, it will run until its maturity date, but you cannot renew it. This was a strategic move to limit the government’s direct liability regarding physical gold prices.

Therefore, any new participation in the Gold monetization scheme by Indian government and banks in 2026: HOW TO earn from physical gold must be done exclusively through bank-managed short-term options.

Is GMS Government Protected?

A common question I get from new investors is: “If I give my physical gold to a bank, is it safe?”

The short answer is yes, but with specific limits. Because the RBI ended the Medium and Long-Term Government Deposits, your new deposits are held directly by the commercial banks.

However, just like your regular savings account or fixed deposit, your GMS account is protected by the Deposit Insurance and Credit Guarantee Corporation (DICGC), an RBI subsidiary. The DICGC covers bank deposits up to ₹5 Lakhs per bank.

If you are depositing 100 grams of gold, calculate its current market value. If it falls under the ₹5 Lakh limit, your capital is completely insured by the RBI framework. For deposits larger than ₹5 Lakhs, you are relying on the fundamental financial strength of the bank—which is why choosing the right banking partner is critical.

What Types of GMS Schemes Are Active in 2026

Since the RBI discontinued the longer-term government deposits, there is only one active scheme category in 2026: Short Term Bank Deposits (STBD).

STBD Features:

- Tenure: 1 to 3 years.

- Interest Rate: Determined by the individual banks. Usually, it ranges between 0.50% to 1.50% per annum.

- Lock-in: Most banks have a minimum 1-year lock-in period. If you withdraw early, you will face a penalty on the interest earned.

- Issuer: The bank itself (not the Central Government).

This short-term nature is actually beneficial for financial planning. It keeps your asset allocation liquid. If gold prices spike significantly, a 1-to-3-year tenure allows you to exit and book profits much faster than the old 15-year lock-ins.

Top 10 Banks Supporting GMS

Not every small bank has the infrastructure to handle the Gold monetization scheme by Indian government and banks in 2026: HOW TO earn from physical gold. You need a bank with a strong treasury and partnerships with CPTCs.

Based on current RBI authorizations, here are the top banks you should approach:

- State Bank of India (SBI)

- HDFC Bank

- ICICI Bank

- Bank of Baroda

- Punjab National Bank (PNB)

- Axis Bank

- Kotak Mahindra Bank

- Union Bank of India

- Indian Overseas Bank (IOB)

- Federal Bank

Pro Tip: Before carrying your gold, call the specific branch. Usually, only specialized main branches in tier-1 and tier-2 cities handle GMS processing directly.

Pros & Cons

Like any financial product—whether it is a high-NAV mutual fund or an equity share—GMS has distinct advantages and disadvantages. Let’s look at the data.

Pros:

- Generates Passive Income: Instead of paying locker fees, your gold pays you up to 1.5% annually.

- Zero Storage Cost: The bank handles security. You save ₹2,000 to ₹5,000 annually on locker rent.

- Purity Upgrade: Old 18K or 22K jewelry is refined into 995-pure 24K gold on your ledger.

- Tax Free: This is the biggest benefit. All interest earned and capital appreciation is completely tax-free (more on this below).

Cons:

- Loss of Making Charges: When you melt jewelry, the 10-20% you paid for making charges is gone forever.

- Emotional Loss: You cannot get your grandmother’s necklace back. It is melted.

- Low Interest: Compared to the stock market or a debt mutual fund, 1.5% is low (though it is paid on top of the gold price appreciation).

- Process Friction: Visiting a CPTC and waiting for testing is far more tedious than buying a Gold ETF on your phone.

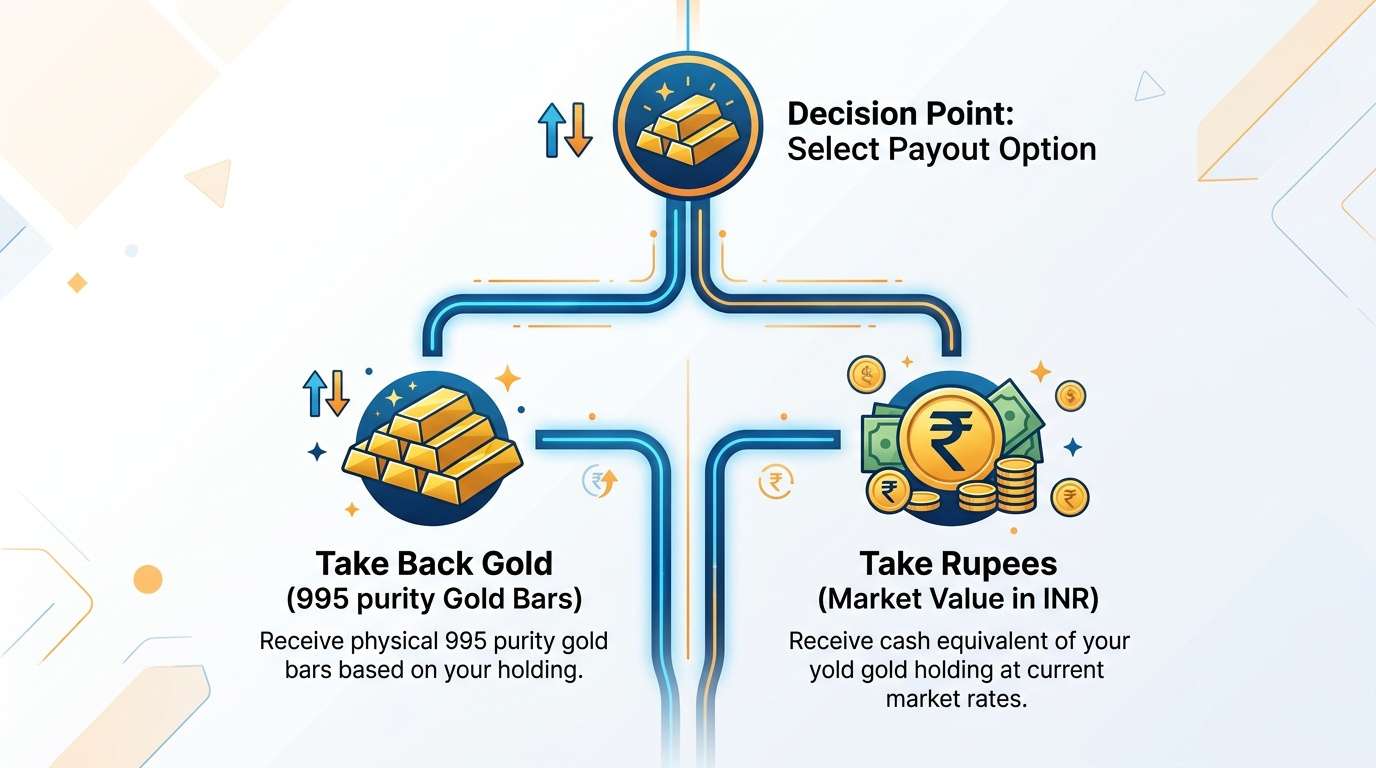

What Happens at Maturity

When you open your STBD account, the bank will ask you a critical question: Do you want your maturity proceeds in cash or in physical gold?

You must decide this at the time of deposit.

- If you choose Cash: On maturity, the bank will check the exact market price of gold on that specific day and credit the INR equivalent directly into your savings account.

- If you choose Gold: The bank will return physical gold (usually in the form of 995 fineness gold bars or coins) equivalent to your deposit weight plus the interest earned. Note that fractional interest might still be paid in cash.

In my experience, if you are using this for long-term wealth preservation, always opt to receive physical gold at maturity. If you take cash, you might spend it, disrupting your overall portfolio asset allocation.

Tax on Interest & Maturity in 2026

Taxation is where the GMS truly outshines physical gold hoarding.

If you keep gold coins in your locker and sell them after 5 years, you will pay Long-Term Capital Gains (LTCG) tax of 12.5% on your profits.

However, under the Gold monetization scheme by Indian government and banks in 2026: HOW TO earn from physical gold, the Income Tax Act provides massive exemptions:

- Zero Capital Gains Tax: When your GMS deposit matures, the profit you make from the rise in gold prices is 100% tax-free. No STCG, no LTCG.

- Zero Income Tax on Interest: The 1.5% annual interest you earn is exempt from income tax, regardless of your tax slab.

- No Wealth Tax: The deposit is exempt from wealth tax assessments.

This makes GMS one of the most tax-efficient instruments in the Indian financial ecosystem.

What If a Bank Can’t Pay — Gold or Money?

Let’s address the worst-case scenario. What if the bank goes bankrupt?

As mentioned earlier, your deposit is covered by DICGC insurance up to ₹5 Lakhs. If you deposited gold worth ₹4 Lakhs, the DICGC ensures you get your equivalent monetary value back.

But what if your deposit is worth ₹20 Lakhs? For amounts over ₹5 Lakhs, you technically become an unsecured creditor to the bank. However, in the Indian context, the RBI closely monitors Scheduled Commercial Banks. Systemic failure of a major bank like SBI, HDFC, or ICICI is historically unprecedented. The RBI usually forces mergers to protect depositors long before a bank completely defaults.

To mitigate risk, if you have 500 grams of gold, split it across multiple banks (e.g., 100 grams in SBI, 100 grams in HDFC). This maximizes your DICGC coverage.

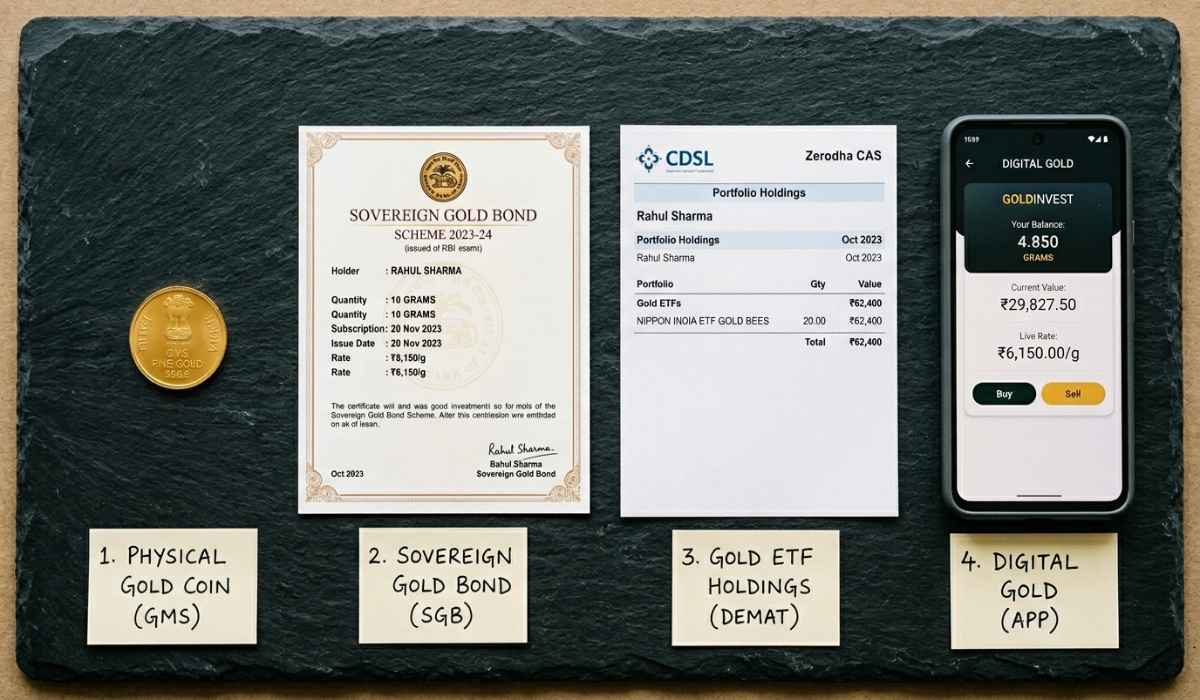

GMS vs Gold ETFs vs Sovereign Gold Bonds vs Gold Mutual Funds vs Digital Gold

How does GMS compare to other gold products? Let’s break down the data.

| Feature | GMS | Gold ETFs / Mutual Funds | Sovereign Gold Bonds (SGB) | Digital Gold |

| Best For | People who already own physical idle gold. | Fresh investments via SIP. High liquidity. | Fresh investments for long-term (8 years). | Tiny fractional buys (e.g., ₹100). |

| Underlying Asset | Your old physical gold. | Digital units backed by physical gold. | Government debt linked to gold price. | Physical gold stored in a vault by a startup. |

| Interest Earned | Yes (0.5% – 1.5%). | No (Only price appreciation). | Yes (2.5% historically). | No. |

| Regulation | RBI / Banks. | SEBI. | RBI / Government. | Unregulated / Evolving. |

| Taxation | Completely Tax-Free. | LTCG of 12.5% after 24 months. | Tax-free if held till maturity. | Taxed as physical gold. |

| 2026 Status | Active (STBD only). | Active (Easy to buy on NSE/BSE). | Paused for new issues. | Active but risky. |

The Decision Framework:

- If you have old, broken jewelry and want to earn passive income while saving locker fees, choose GMS.

- If you have fresh INR cash and want to do a monthly SIP to diversify your equity portfolio, choose a Gold Mutual Fund or Gold ETF. You can track the NAV daily, and the expense ratio is very low.

- Note on SGBs: While SGBs were previously the best tool for fresh cash, the government has discontinued new issues for 2025-2026. Therefore, ETFs are your best bet for fresh money today.

Conclusion

Let’s wrap up exactly what we have learned about unlocking your dead assets today:

- Turn Idle Gold into Cash: The GMS allows you to melt unwanted, non-emotional physical gold to earn an annual interest of up to 1.5%.

- Short-Term Focus in 2026: With the RBI ending long-term deposits, you can safely lock your gold in 1-to-3-year Short Term Bank Deposits (STBD).

- Massive Tax Benefits: Both your interest income and your capital appreciation on maturity are 100% tax-free.

- Not for Fresh Investments: Use GMS only to recycle existing physical gold. If you have fresh cash, buy a Gold ETF on the stock exchange instead.

In financial planning, every rupee counts, and every asset must work for you. Leaving gold in a locker to gather dust while paying bank fees is a major financial mistake. Look inside your vault, separate the emotional jewelry from the investment gold, and put that capital to work.

Start treating your gold like the financial asset it was always meant to be. Take control, stay updated with the data, and build wealth that outlasts you.

Also Read: After SpaceX’s Bumper Listing, Can Indian Investors Subscribe to IPOs from USA?

Disclaimer: This article is for educational purposes only and does not constitute financial or investment advice; consult a SEBI-registered advisor before making any decisions. The Gold Monetization Scheme involves risks including irreversible jewelry melting, bank default beyond DICGC limits, and variable interest rates. All information is accurate as of June 2026 — verify the latest terms with your bank or the RBI’s official website before participating.