Why do so many Indians celebrate a profitable property sale, only to panic when they see their tax bill?

During my 5+ years working at ICICI Prudential, I sat across the table from countless clients who had just sold a house or a piece of land. They were thrilled about the big payday. But when their Chartered Accountant calculated the Long-Term Capital Gains (LTCG) tax, their smiles quickly vanished. Many were forced to hand over lakhs of their hard-earned profits to the taxman simply because they didn’t plan ahead.

If you have recently sold a property, you might be staring at a massive tax liability. But here is the good news: you do not have to lose a huge chunk of your profits. By utilizing Section 54EC of the Income Tax Act, you can legally shield your money by investing in Capital Gain Bonds.

In my 14 years of actively investing and advising in the financial sector, I have seen how a lack of awareness destroys wealth. Today, as the founder of PaisaForever, my mission is to give you the exact, data-driven facts you need. In this guide, you will learn exactly how the tax on property sales works in AY 2026-27, how Section 54EC bonds operate, and the exact steps to protect your real estate profits.

Let’s dive in.

The Tax Problem on Property Sale

Before we can solve the problem, we need to understand exactly how much the government takes when you sell real estate. In India, when you sell a capital asset like a house or land for a profit, that profit is taxed as a Capital Gain.

Current LTCG Tax Rate in AY 2026-27

Following recent budget updates, the taxation landscape for property sales has shifted. If you hold a property for more than 24 months, it is considered a long-term asset. For the Assessment Year (AY) 2026-27, the standard Long-Term Capital Gains (LTCG) tax rate is 12.5% without indexation.

However, there is a grandfathering clause. If you purchased your property before July 23, 2024, the government gives you an option: you can either pay 12.5% without indexation, OR you can pay 20% with indexation—whichever results in a lower tax bill.

(Note: Indexation is simply a method that adjusts your property’s original purchase price for inflation, legally reducing your taxable profit).

Realistic Examples of Tax on Property Sales

Let’s look at the numbers. Suppose you bought a plot of land for ₹50 lakh and sold it for ₹1.5 crore after five years.

- Without Indexation: Your pure profit is ₹1 crore. At the flat 12.5% rate, your tax liability is a staggering ₹12.5 lakh.

Impact of Tax on Net Proceeds

Losing ₹12.5 lakh from your net proceeds is a massive blow. That is money you could have used for your child’s education, added to your retirement corpus, or invested in a diversified portfolio. When sellers realize the sheer size of this tax leak, they scramble for exemptions. This is exactly where Section 54EC comes into play to rescue your capital.

Overview of Section 54EC

When I analyze wealth-building strategies for PaisaForever readers, I always emphasize legal tax efficiency. Section 54EC of the Income Tax Act is one of the most powerful tools provided by the government to help you save your real estate profits.

Purpose of Section 54EC

The primary purpose of Section 54EC is to encourage taxpayers to reinvest their capital gains into infrastructure development. Instead of taking tax money from you, the government allows you to lend that money to state-backed infrastructure companies.

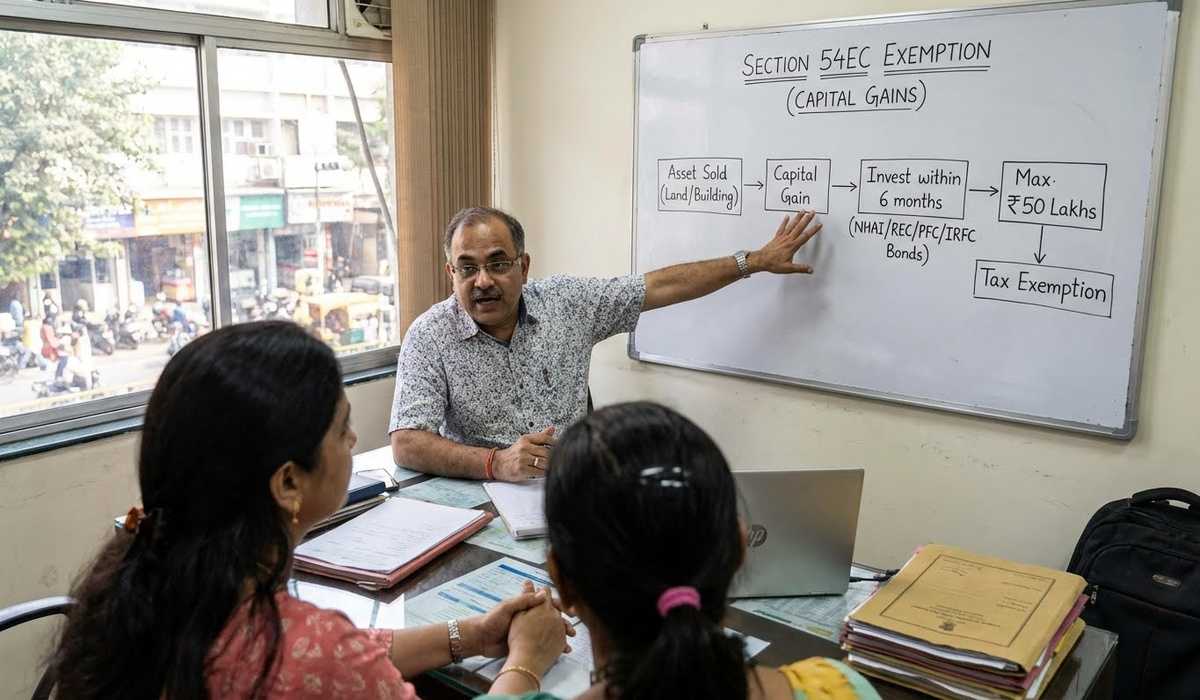

How it Provides Exemption on Long-Term Capital Gains

If you reinvest your capital gains into specifically notified “Capital Gain Bonds” within a set timeframe, the amount you invest becomes entirely tax-exempt.

Basic Mechanism of Investing

The mechanism is straightforward: You calculate your long-term capital gain, take that profit, and buy these specified bonds. By doing so, the taxable gain is legally erased up to the amount invested.

Key Benefit Compared to Paying Tax

The biggest benefit is wealth preservation. Instead of paying a 12.5% or 20% non-refundable tax to the government, you retain 100% of your principal amount. Plus, you earn a fixed annual interest on these bonds. It is a dual advantage: you save tax today and generate passive income tomorrow.

Eligibility Conditions

Not every transaction qualifies for this exemption. Over my 10+ years in the Indian stock market and personal finance space, I’ve seen people assume they can buy these bonds after selling shares or mutual funds. That is a costly misconception.

Type of Asset That Qualifies

Section 54EC strictly applies only to land or building or both. You cannot claim this exemption if you sell gold, equity shares, machinery, or cryptocurrency.

Minimum Holding Period

To qualify for 54EC, the property sold must be a long-term capital asset. In India, real estate qualifies as long-term if you have held it for more than 24 months before selling. If you flip a property within 18 months, the profit is a Short-Term Capital Gain (STCG), taxed at your normal income slab rate, and 54EC bonds will not save you.

Who Can Claim the Exemption?

Any taxpayer can claim this exemption. This includes Individuals, Hindu Undivided Families (HUFs), Partnership Firms, and Companies.

Restrictions for NRIs

Non-Resident Indians (NRIs) are also fully eligible to invest in 54EC bonds to save tax on property sold in India. However, NRIs must navigate strict TDS (Tax Deducted at Source) rules. When an NRI sells property, the buyer must deduct TDS at 20% (or 12.5%) on the entire capital gain. To avoid this, the NRI must apply for a Lower Deduction Certificate from the Income Tax Department before the sale, proving their intent to invest in 54EC bonds.

Investment Timeline

In finance, timing is everything. Missing a deadline by a single day can cost you lakhs.

Exact Time Limit

To claim the exemption under Section 54EC of the Income Tax Act, you must invest the capital gains into the approved bonds within 6 months (strictly) from the date of transfer of the property.

Date from Which the Period is Calculated

The “date of transfer” is generally the date the sale deed is registered. If you sold your house on January 10th, your 6-month window starts ticking immediately from that exact date.

Consequences of Missing the Deadline

If you try to invest on the 6th month and 1st day, the Income Tax Department will reject your exemption. Your entire capital gain will become fully taxable, along with applicable penalties and interest if you missed your advance tax payments.

Applicability of Capital Gains Account Scheme

Here is a vital distinction: For other tax exemptions (like buying a new house under Section 54), you can park your money temporarily in a Capital Gains Account Scheme (CGAS) before the ITR filing due date. This does NOT apply to Section 54EC. You cannot use the CGAS to extend your 6-month deadline. You must buy the actual bonds within those 6 months.

Eligible Bonds and Issuers

You cannot buy just any bond in the market to save this tax. The government explicitly notifies which bonds qualify as “long-term specified assets.”

List of Approved Issuers

Currently, you can invest in 54EC bonds issued by the following government-backed entities:

- REC bonds (Rural Electrification Corporation)

- NHAI bonds (National Highways Authority of India)

- PFC bonds (Power Finance Corporation)

- IRFC bonds (Indian Railway Finance Corporation)

- HUDCO (Housing and Urban Development Corporation)

- IREDA (Indian Renewable Energy Development Agency) – Recently added in 2025 to boost green energy funding.

Current Interest Rate

Currently, these Capital Gain Bonds offer a fixed interest rate of 5.25% per annum. The interest is paid out annually to your bank account. Keep in mind, while the bond saves you from capital gains tax, the 5.25% interest you earn every year is fully taxable as per your regular income tax slab.

Credit Rating and Safety Features

As a former ICICI Prudential insider, I always look at risk first. These bonds are exceptionally safe. They carry a “AAA” credit rating from top agencies like CRISIL, CARE, and ICRA. Because they are backed by the central government, the default risk is virtually zero.

Investment Limit and Tax Savings

While the government wants to help you save tax, they put a cap on how much you can shelter.

Maximum Investment Limit

Under Section 54EC of the Income Tax Act, the maximum amount you can invest in these bonds is ₹50 lakh per financial year.

Limit per PAN

This limit is tied to your PAN card. You cannot invest ₹50 lakh in NHAI and another ₹50 lakh in REC. The total aggregate investment across all eligible bonds cannot exceed ₹50 lakh in a single financial year. Furthermore, the law prevents you from splitting the 6-month window across two financial years to claim ₹1 crore. The maximum exemption for a single property transaction is capped at ₹50 lakh.

Tax Saved on ₹50 Lakh Investment

Let’s look at the data. If you have ₹50 lakh in capital gains and invest it entirely in 54EC bonds:

- Under the 12.5% rule: You instantly save ₹6,25,000 in taxes.

- Under the 20% rule (with indexation): You save ₹10,000,000 in taxes.

Treatment When Capital Gains Exceed the Limit

If your long-term capital gain is ₹80 lakh, you can only invest a maximum of ₹50 lakh in 54EC bonds. The remaining ₹30 lakh will be taxed at the applicable LTCG rate (12.5% or 20%), unless you use other exemptions like Section 54 (buying a new residential house).

Exemption Calculation

Calculating your exemption is straightforward, but clarity is crucial when filing your ITR.

How Exemption Amount is Determined

The law states that the exemption is equal to the amount invested in the bonds, up to the maximum limit of ₹50 lakh.

Full Investment Scenario

Scenario: You sold an apartment. Your calculated LTCG is ₹30 lakh.

- You invest ₹30 lakh in REC 54EC bonds within 6 months.

- Taxable Gain: ₹30L – ₹30L = Zero. You pay no tax.

Partial Investment Scenario

Scenario: Your LTCG is ₹40 lakh, but you need liquidity, so you only invest ₹25 lakh in NHAI bonds.

- Taxable Gain: ₹40L – ₹25L = ₹15 lakh. * You will pay 12.5% tax on the remaining ₹15 lakh (plus cess/surcharge).

Scenario When Gains Exceed ₹50 Lakh

Scenario: You sold a commercial plot with a massive LTCG of ₹90 lakh.

- You invest the maximum permissible limit of ₹50 lakh in HUDCO bonds.

- Taxable Gain: ₹90L – ₹50L = ₹40 lakh.

- You must pay LTCG tax on the ₹40 lakh balance.

Lock-in Period and Conditions

These bonds are not meant for short-term liquidity. You are trading your liquidity for a massive tax break.

Duration of the Lock-in Period

As per current tax laws, 54EC Capital Gain Bonds come with a strict 5-year lock-in period (60 months). Previously, this lock-in was 3 years, but it was extended to 5 years starting from April 2018.

Prohibited Actions During Lock-in

During this 5-year period, your money is completely illiquid.

- You cannot sell the bonds on the secondary market.

- You cannot transfer them to another person.

- Most importantly, you cannot pledge them as collateral to get a loan from a bank.

Consequences of Violating the Conditions

If you attempt to bypass these rules—for example, if a bank mistakenly grants you a loan against these bonds within the 5-year window—the Income Tax Department will penalize you.

Tax Treatment on Violation

The moment you violate the lock-in condition, the original tax exemption is instantly revoked. The amount you initially claimed as an exemption will be treated as long-term capital gains in the year of the violation, and you will be forced to pay the tax you originally avoided, along with heavy penalty interest.

Investment Process

As someone who helps people build robust portfolios, I assure you that investing in these bonds is a painless process.

Where and How to Apply

You can invest in 54EC bonds through authorized banks (like HDFC, SBI, ICICI) or through registered stockbrokers. You can fill out a physical form or apply online through the bond issuer’s website or your broker’s digital portal.

Documents Required

You will need:

- A copy of your PAN Card

- Aadhaar Card or address proof

- A cancelled cheque of your bank account (for interest payouts)

Payment and Allotment Process

Payment is usually made via a demand draft, cheque, or electronic transfer (NEFT/RTGS). Once the funds clear, the issuer will process your application. The bonds are typically allotted on the last day of the month in which your funds are credited to their account.

Physical vs Demat Holding

You have the choice to hold these bonds in physical form (as a certificate) or in your Demat account. Given my 10+ years in the stock market, I strongly advise holding them in Demat form. It prevents the loss of physical certificates, makes address changes seamless, and ensures the maturity amount hits your bank account automatically after 5 years.

Claiming Exemption in Income Tax Return

When you file your ITR for the financial year in which the sale occurred, you must explicitly report your total capital gains under the “Capital Gains” schedule. There will be a specific row to claim deductions under Section 54EC. You will enter the invested amount and the details of the bonds to reduce your taxable income.

Compare Section 54EC vs Section 54 vs Section 54F

Sellers often confuse the different property tax exemptions. Here is a clear comparison framework:

| Feature | Section 54 | Section 54F | Section 54EC |

| What did you sell? | Residential House | Any asset EXCEPT a residential house (e.g., land, gold) | Land or Building (Residential or Commercial) |

| Where must you invest? | A new residential house | A new residential house | Specified Bonds (REC, NHAI, PFC, etc.) |

| What amount must be invested? | Only the Capital Gain | The entire Net Sale Consideration | Only the Capital Gain |

| Time Limit | Purchase within 1 yr before or 2 yrs after; Construct within 3 yrs | Purchase within 1 yr before or 2 yrs after; Construct within 3 yrs | Strictly within 6 months from the date of sale |

| Maximum Limit | Up to ₹10 Crore | Up to ₹10 Crore | Maximum ₹50 Lakh per Financial Year |

| Lock-in Period | 3 Years | 3 Years | 5 Years |

| Best Suited For… | Sellers upgrading to a new home | Sellers moving from land/commercial to a residential home | Sellers who want passive income, avoid real estate hassle, and have gains up to ₹50L |

Key Takeaways and Precautions

When it comes to financial planning, the details dictate your success. Before you deploy your money, keep these things in mind:

Common Mistakes to Avoid

- Missing the 6-month deadline: I have seen investors wait until ITR season to think about tax planning. By then, the 6-month window is often closed. Do not delay.

- Assuming interest is tax-free: The 5.25% interest is added to your taxable income. If you are in the 30% bracket, your post-tax return is lower.

- Applying for loans: Never pledge these bonds during the 5-year lock-in.

Advantages of This Route

Section 54EC of the Income Tax Act provides a hassle-free, guaranteed way to protect up to ₹50 lakh of your wealth without the physical maintenance, stamp duty, or tenant issues associated with buying a new property.

Situations Where This Option is Suitable

This route is perfect for retirees, HNIs, or anyone who has recently sold property, does not want to reinvest in real estate, and prefers preserving their capital in a sovereign-backed, low-risk instrument.

Important Reminders

- Always calculate whether paying the 12.5% tax and investing the balance in high-growth assets (like equity mutual funds via SIP) yields better long-term results than locking the money at 5.25% for 5 years. Do the math based on your risk appetite!

Conclusion

Let’s recap what you have learned today:

- The current LTCG on property is 12.5% (or 20% with indexation for older properties), which can eat a massive hole in your net proceeds.

- Section 54EC allows you to completely wipe out tax on up to ₹50 lakh of gains by investing in secure, AAA-rated bonds.

- You must act swiftly—the investment must be completed within exactly 6 months of your property sale.

- While the principal is locked for 5 years safely, the 5.25% annual interest you earn is taxable.

At PaisaForever, I believe that it is not just about how much money you make; it is about how much money you keep. Do not let ignorance lead to an unnecessary tax leak. Evaluate your net gains, assess your liquidity needs for the next five years, and if it aligns with your financial plan, utilize Capital Gain Bonds to secure your wealth.

Take control of your money, consult with your tax advisor, and invest wisely!

Also Read: Gold Monetization Scheme: How to earn from Physical Gold in 2026